The rollout of GST 2.0 in September 2025 represents a defining moment in India’s indirect taxation framework. This reform aims to simplify tax structures, rationalize rates, and resolve long-standing inefficiencies, with a strong focus on youth-driven sectors of the economy. By reducing the tax burden across industries such as education, healthcare, technology, textiles, food processing, and automobiles, GST 2.0 seeks to encourage entrepreneurship, generate employment, and make essential goods and services more affordable. The reform not only delivers immediate financial relief but also strengthens India’s vision of inclusive and sustainable economic growth.

GST 2.0 Comes into Effect

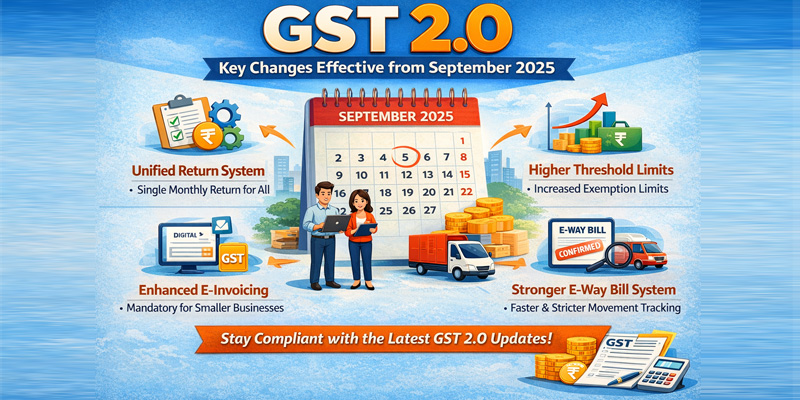

On 22 September 2025, the next-generation GST framework formally came into force. Announced during the Prime Minister’s Independence Day address and finalized at the 56th GST Council meeting, GST 2.0 has been positioned as a comprehensive overhaul of the existing system. Its objective is to reduce household expenditure, improve affordability in healthcare and insurance, and provide timely relief for farmers, manufacturers, and consumers. By making compliance simpler and the system more transparent, GST 2.0 is expected to enhance efficiency and stimulate economic activity during the festive season and beyond.

Core Reforms under GST 2.0

The new structure introduces significant rationalisation of tax slabs, along with administrative improvements aimed at supporting ease of doing business. Key highlights include:

- Simplified Rate Structure – Reduction of multiple tax slabs to just two primary rates, along with exemptions for essentials and higher taxes on luxury/sin goods.

- Industry-Specific Relief – Lowered GST rates for sectors such as textiles, footwear, handicrafts, logistics, and packaging to support small businesses and startups.

- Inverted Duty Correction – Elimination of mismatched tax rates that previously discouraged investment and manufacturing.

Together, these measures reduce costs for consumers, enhance competitiveness for domestic businesses, and provide stronger incentives for entrepreneurship.

GST Rate and Slab Restructuring

0% GST – Essentials and Insurance

A landmark change in GST 2.0 is the exemption of essential goods and critical services. The 0% category includes:

- Food staples such as milk, bread, and chapatis.

- Basic educational materials like pencils, erasers, and maps.

- Life and health insurance premiums.

- Life-saving medicines, including 33 cancer drugs.

This exemption directly lowers healthcare and education costs while reducing the overall cost of living.

5% GST – Common Essentials

The 5% slab now applies to items of everyday use and agricultural inputs, such as:

- Dairy products, dry fruits, biscuits, and juices.

- Personal care products like soaps, shampoos, and toothpaste.

- Agricultural machinery including tractors and harvesters.

- Environment-friendly products such as bio-pesticides.

These reductions make farming more cost-effective and consumer products more affordable, particularly benefiting rural households.

18% GST – Standard Rate

The 18% slab has been designated as the standard rate, covering a broad range of goods and services, including:

- Electronics and appliances such as televisions (up to 32 inches), dishwashers, and air conditioners.

- Automobiles including motorcycles up to 350cc and commercial vehicles.

- Cement, reduced from 28% to 18%, offering significant relief for the construction and real estate sectors.

- Hotel accommodation priced up to ₹7,500 per night.

This rationalisation is expected to provide a boost to infrastructure, tourism, and consumer durables.

40% GST – Sin and Luxury Goods

To promote social equity and discourage non-essential consumption, luxury and sin goods remain heavily taxed at 40%. This category includes:

- Tobacco, alcohol, and related products.

- High-end imported goods, luxury cars, and premium jewelry.

The approach balances affordability of essentials with higher taxation on luxury indulgence.

Administrative Reforms under GST 2.0

In addition to restructuring rates, GST 2.0 introduces key administrative improvements designed to streamline compliance:

- Faster GST Registration: Businesses can now obtain GST registration within three working days, compared to the earlier 7–10 days.

- Automated Refunds: Refund claims up to ₹1,000 crore will be processed electronically, with exporters receiving refunds within seven days of filing.

- Dispute Resolution Mechanism: Strengthened GST tribunals will address over 40,000 pending cases, ensuring faster resolution of disputes and reducing litigation backlog.

These reforms improve liquidity for small and medium enterprises, reduce bureaucratic delays, and enhance the ease of doing business.

Conclusion

GST 2.0 is not merely a revision of tax rates but a holistic restructuring of India’s indirect taxation framework. With its simplified slab system, rationalised rates, and improved compliance mechanisms, the reform delivers relief to households, strengthens industry competitiveness, and creates new opportunities for entrepreneurs and startups. By balancing affordability of essentials with higher taxation on luxury consumption, GST 2.0 lays the foundation for a more inclusive, transparent, and growth-oriented economy.

If you have any further questions or need assistance, feel free to reach out to us at admin@ushmaassociates.com or info@nricaservices.com, or contact us via call/WhatsApp at +91 9910075924.

Stay Updated, Stay Compliant!

Disclaimer: Aim of this article is to give basic knowledge about the topic to people who are not in touch with Indian tax norms. When anybody is dealing with these kinds of cases practically, he shall consider all relevant provisions of all applicable Laws like FEMA/Income Tax/RBI /Companies Act etc.